OKO's CEO Simon Schwall was invited to reflect on the regulatory environment in Africa, 8 years after receiving the Allliance for Financial Inclusion (AFI) fintech showcase award. He is sharing his thoughts below:

Try selling a parametric drought insurance policy:

❌ in a language with no word for “insurance”

❌ to a farmer with low financial literacy,

❌ and only reacheable after 2 hours of driving in the mud

That deserves a bonus, right?😅

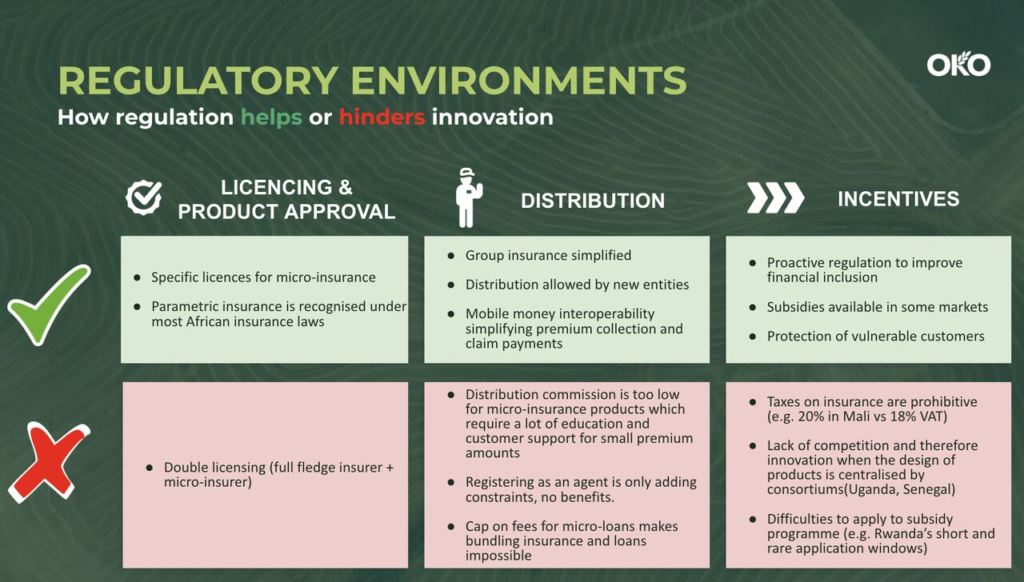

Well, the regulators don't seem to agree. Look at these friction points:

- Uganda: Commissions for distributors are capped at a tight 10%.

- Mali: Insurance product tax sits at 20% (while VAT is only 18%).

- West Africa (CIMA region): Want to sell "micro-insurance"? You need to apply for an entirely separate, additional license.

But it’s not all uphill. The tide is turning:

🌾 Parametric insurance is finally being recognized as the solution across most African countries.

📱 Mobile Money interoperability is making it seamless to collect tiny premiums. 🇸🇳 Forward-thinking countries like Senegal have entirely lifted taxes on crop insurance.

Thank you, AFI, for the platform and for your tireless work promoting #FinancialInclusion!

At OKO Finance, we’ve always believed in the transformative power of climate insurance for smallholder farmers. From food security to financial stability, the right tools can help farming communities adapt to a changing climate while building brighter futures.

In collaboration with USAID, we were preparing to launch three ambitious, high-impact initiatives across Mali, the Democratic Republic of Congo (DRC), and Côte d’Ivoire. Each project was designed not only to improve resilience against climate shocks, but also to unlock income opportunities and strengthen local economies.

Unfortunately, all three projects were abruptly halted following the Trump administration’s decision to shut down several USAID programs in 2020, a policy shift that affected development efforts around the world.

But while this setback stalled implementation, it also created an exceptional opportunity: these projects are still viable, thoroughly developed, and ready for execution, awaiting new partners to bring them to life.

The Three Projects interrupted and ready to be revived

1. Rural Training and Youth Empowerment in Mali

This initiative was designed to build awareness among farmers about climate insurance, while also creating employment opportunities for rural youth. By training young people as insurance distribution agents, the program addressed two major challenges at once: climate vulnerability and rural unemployment.

With training modules, outreach strategies, and local partnerships already mapped out, the program is ready for immediate launch.

2. Launching Maize Insurance in the Democratic Republic of Congo

In the DRC, our partnership with USAID aimed to introduce index-based insurance products for maize farmers, helping them cope with drought and erratic weather patterns. This would have been OKO’s first rollout in Central Africa — a crucial expansion in a country where farmers are increasingly exposed to climate risks.

All product design work, pricing models, and pilot frameworks are completed and ready to be implemented.

3. Expanding Insurance Coverage in Côte d’Ivoire

This initiative was set to deliver tailored insurance for key Ivorian crops: coffee, cashew, cassava, and rice. Expanding beyond our existing offerings, this project would have significantly scaled OKO’s reach and supported the country’s agricultural backbone.

Validated by local stakeholders and supported by feasibility studies, the project is well-positioned for rapid deployment.

In recent years, mobile technology has revolutionized various sectors across Africa, and agriculture is no exception. Among the many benefits it brings, one of the most significant is improved access to insurance for African farmers. This development is important for a continent where agriculture is a primary source of livelihood for millions. Mobile technology not only facilitates communication and access to information but also provides a platform for innovative financial solutions that can mitigate risks and enhance productivity for farmers.

The importance of insurance for african farmers

Agriculture in Africa faces numerous challenges, including unpredictable weather patterns, pests, diseases, and market volatility. These factors contribute to a high level of uncertainty and risk, which can significantly impact farmers' livelihoods. Insurance plays a vital role in managing these risks by providing financial protection against potential losses. However, traditional insurance products have been largely inaccessible to smallholder farmers due to high costs, lack of awareness, and logistical challenges. Mobile technology is now bridging this gap, making access to insurance for African farmers more feasible and affordable.

Mobile technology as a game-changer

Mobile technology has emerged as a transformative force, dramatically altering the landscape of agricultural insurance in Africa by increasing connectivity and enabling the creation of innovative insurance products.

Increased penetration and connectivity

One of the key reasons mobile technology is transforming access to insurance for African farmers is the rapid increase in mobile phone penetration across the continent. According to the GSMA, over 50% of the population in sub-Saharan Africa now has a mobile subscription. This widespread connectivity allows insurers to reach farmers in remote areas who were previously excluded from formal financial services.

Innovative insurance products

Mobile technology has enabled the development of innovative insurance products tailored to the needs of smallholder farmers. For instance, weather index insurance, which pays out benefits based on weather conditions rather than actual crop loss, is gaining popularity. Farmers can purchase and receive payouts for these insurance products via their mobile phones, making the process simple and efficient. This innovation is a significant step forward in enhancing access to insurance for African farmers.

Also read : How agricultural insurance can transform small farms in Africa

Case studies: success stories

OKO finance in Mali and Uganda

A prime example of mobile technology improving access to insurance for African farmers is the innovative approach of OKO Finance. Operating in countries like Mali and Uganda, OKO Finance leverages mobile technology to offer weather index insurance products specifically designed for smallholder farmers. This service aims to protect farmers against the financial impact of adverse weather conditions, such as droughts and excessive rainfall, which are common in these regions.

OKO Finance utilizes satellite data to monitor weather conditions and automatically trigger payouts when predefined weather events occur. This method ensures that the process is transparent and efficient, eliminating the need for lengthy claims processes. Farmers can enroll in the insurance program, pay premiums, and receive payouts all through their mobile phones, making the system highly accessible even in remote areas.

By partnering with local mobile network operators and financial institutions, OKO Finance has successfully expanded its reach, providing insurance coverage to thousands of farmers who were previously underserved. This initiative not only helps farmers to secure their livelihoods but also encourages investment in better farming practices and inputs, knowing they have a financial safety net.

OKO Finance's success in using mobile technology to enhance access to insurance for African farmers illustrates the transformative potential of digital solutions in agriculture. The company's innovative approach serves as a model for other regions and sectors, demonstrating how technology can bridge the gap between traditional insurance products and the needs of smallholder farmers.

The role of mobile money

In Uganda and Mali, mobile money services have played a crucial role in enhancing access to insurance for African farmers. These services allow farmers to make premium payments and receive payouts seamlessly through their mobile phones. For instance, platforms like MTN Mobile Money and Orange Money enable farmers to conduct financial transactions with ease, directly integrating with insurance products offered by companies like OKO Finance.

The integration of mobile money with insurance products reduces transaction costs and makes the entire process more transparent and accessible. Farmers can pay their insurance premiums and receive compensation for claims quickly and efficiently, without needing to travel long distances or deal with cumbersome paperwork. This convenience encourages more farmers to invest in insurance, providing them with a financial safety net to protect their crops and livestock against adverse conditions.

As a result, mobile money services have significantly increased the adoption of insurance among smallholder farmers in Uganda and Mali, demonstrating the transformative potential of combining mobile technology with financial services to support agricultural development.

Challenges and future prospects

While mobile technology has significantly improved access to insurance for African farmers, there are still hurdles that must be overcome to fully realize its potential and ensure widespread adoption.

Overcoming barriers

Despite the progress made, several challenges still hinder the widespread adoption of mobile-based insurance solutions. These include limited digital literacy among farmers, inadequate infrastructure in remote areas, and regulatory hurdles. To overcome these barriers, stakeholders, including governments, insurers, and mobile network operators, need to collaborate and invest in education and infrastructure development. Additionally, creating more awareness about the benefits of insurance is essential to encourage more farmers to participate.

The path forward

The future of mobile technology in enhancing access to insurance for African farmers looks promising. With ongoing advancements in technology and increasing investment in digital infrastructure, the potential for growth is immense. Innovations such as blockchain for secure transactions, artificial intelligence for personalized insurance products, and satellite data for accurate weather forecasting will further enhance the effectiveness of mobile-based insurance solutions.

Mobile technology is undeniably a game-changer in improving access to insurance for African farmers. While challenges remain, the continued collaboration between stakeholders and ongoing technological advancements hold great promise for the future. As mobile technology continues to evolve, it will play an increasingly vital role in securing the livelihoods of millions of African farmers, ensuring they can thrive despite the uncertainties of agriculture.

Agriculture is the economic backbone of many African countries, providing employment and livelihoods for a significant portion of the population. However, small-scale farms often face considerable challenges, including climatic risks, crop diseases, and market price fluctuations. In this context, agricultural insurance emerges as a potential solution to transform these small farms, making them more resilient and prosperous. This article explains how agricultural insurance can play a key role in the transformation of small farms in Africa.

Understanding the Challenges of Small-Scale Farming

Small-scale farming faces in Africa faces many challenges. Among them, we have :

Climatic and environmental risks

Small farms in Africa are particularly vulnerable to climatic hazards such as droughts, floods, and storms. These events can destroy entire harvests, jeopardizing farmers' livelihoods and exacerbating poverty. For example, a prolonged drought can lead to significant yield loss, leaving farmers unable to repay loans or invest in the next planting season.

Also read : OKO Takes Home the Insurtech Insights Europe Ambitious Insurer Award

Crop diseases and pests

Diseases and pests represent another major challenge for small farms. Pests like locusts can devastate crops, while diseases can significantly reduce yields. Without adequate means to combat these threats, farmers find themselves in a precarious situation where a single outbreak can wipe out their efforts and investments.

Limited access to markets and financing

Small-scale farmers also suffer from limited access to markets and financing. They often struggle to sell their products at fair prices or obtain loans to improve their agricultural practices. This situation is worsened by the lack of financial support mechanisms, which limits their ability to invest in more resilient technologies or practices.

What is the role of agricultural insurance?

Protection against financial losses

Agricultural insurance provides financial protection against losses due to natural disasters, diseases, and other risks. By compensating farmers for crop losses, it allows them to maintain their activities and plan for the future with greater certainty. For example, an insured farmer can receive compensation for a crop destroyed by drought, helping them purchase seeds and plant again.

Facilitating access to credit

Having agricultural insurance can also improve farmers' access to credit. Financial institutions are more willing to lend to insured farmers because insurance reduces the risk of non-repayment. This enables farmers to invest in modern technologies, buy higher-quality inputs, and adopt more sustainable agricultural practices.

Encouraging adoption of innovative technologies and practices

Agricultural insurance can incentivize farmers to adopt innovative technologies and practices. For example, by offering premium discounts to farmers who adopt water conservation practices or use drought-resistant seeds, insurance companies can promote more resilient agricultural practices. This helps improve productivity and reduces vulnerability to climatic hazards.

Also read : Insurtech OKO raises $500,000 USD in an extension round for their expansion to Côte D’Ivoire.

Challenges and opportunities of agricultural insurance in Africa

Implementation challenges

Despite its potential benefits, implementing agricultural insurance in Africa faces several challenges. The lack of accurate data on crop yields and climatic risks makes it difficult to assess risks and set premiums. Additionally, the low penetration of financial services in rural areas and the lack of awareness among farmers about the benefits of insurance pose major obstacles.

Successful initiatives and lessons learned

However, some initiatives have shown promising results. For example, OKO, an agricultural insurance provider, has successfully implemented insurance solutions in countries like Mali and Uganda. OKO uses satellite data to assess crop damage and mobile technologies to facilitate enrollment and premium payments. By leveraging these technologies, OKO has been able to provide affordable and accessible insurance to small farmers, helping them mitigate risks and invest in their farms with greater confidence. This model can be replicated in other African countries with adaptations to local contexts.

Opportunities for the future

The rise of digital technologies and telecommunications offers opportunities to expand agricultural insurance coverage. Mobile applications can facilitate data collection, risk assessment, and indemnity payments, making insurance more accessible and affordable for small farms. Moreover, collaboration between governments, private insurers, and international organizations can create subsidized insurance programs that protect the most vulnerable farmers.

Agricultural insurance has the potential to transform small farms in Africa by offering protection against risks and facilitating access to financing and markets. Although challenges remain, successful initiatives and technological advancements pave the way for broader adoption of agricultural insurance. By supporting small farms, insurance can play a key role in reducing poverty, improving food security, and promoting sustainable agricultural development in Africa.

In a move that resembles a vote of confidence for the start-up, Allianz Africa renewed its multi-year partnership with OKO. Allianz and OKO initially signed an agreement in 2019 to test OKO’s concept in Mali. OKO offered an affordable and automated climate insurance accessible for the first time via mobile phone to smallholder farmers. 4 years later it is the most popular crop insurance in Mali. OKO uses parametric insurance technology, meaning that insurance claims are automatically validated and paid if satellite data shows that the weather conditions were very detrimental to the agricultural activity. It covers events such as droughts and floods.

As previously, the collaboration consists in OKO bringing its data-science expertise and its mobile distribution technology, while Allianz will assist in underwriting and re-insuring the crop insurance products. This new version of the partnership is meant to prepare for geographical expansion to new countries in the continent, and to strengthen the link between the two organizations. In fact, OKO already expanded to Uganda (with Jubilee-Allianz) and Ivory Coast (with Allianz Côte d’Ivoire). OKO and Allianz also won together the Ambitious Insurer award at the 2023 InsurTech Insight conference.

OKO’s activities have also widened, and OKO now works with agro-industrial companies such as AB InBev, Olam and Touton. OKO’s insurance protects farmers from the consequences of droughts and floods, and therefore secures the supply chain for large buyers. OKO also demonstrated its ability to generate positive impact in financial inclusion and climate resilience for vulnerable populations, which helps large food, textile, or beverage companies to achieve their sustainability objectives.

Dans une année marquée par des défis météorologiques, OKO, la start-up

d'assurance agricole basée à Bamako, continue de jouer un rôle essentiel dans la

protection des agriculteurs maliens. Les indemnisations versées cette saison à 2

009 petits exploitants sur les 10 014 assurés témoignent de l'engagement de

l'entreprise envers la résilience face aux aléas climatiques.

Les régions de Ségou et Sikasso ont été durement touchées, avec 1 793

agriculteurs recevant des compensations pour les pertes subies. La carte jointe à

cet article illustre clairement la répartition géographique de ces indemnisations.

Cheick Oumar Tangara, directeur pays chez OKO, souligne l'impact positif de

l'assurance pour la résilience climatique des Agriculteurs ruraux maliens :

"L'objectif d'OKO est d'apporter une solution concrète aux agriculteurs confrontés

aux risques climatiques en leurs offrant un filet de sécurité (financière). Nous

sommes fiers de voir notre assurance jouer un rôle vital pour assurer la stabilité

financière des communautés agricoles."

À ce jour, OKO a assuré 27 000 agriculteurs pour 6 cultures différentes, offrant

une couverture pour le maïs, le sésame, le mil, le sorgho, le coton et l'arachide. Le

système automatisé d'indemnisation par analyse de données satellitaires et le

paiement via Orange Money garantit des compensations rapides lorsque des

conditions météorologiques défavorables sont observées dans les zones agricoles.

Chez OKO, l'accent est mis sur la préparation de la prochaine saison. Les

agriculteurs intéressés pour la saison 2024 sont invités à s'inscrire dès maintenant

en composant le 77 99 80 80 ou en utilisant le code #144#343# sur leur mobiles

Orange.

Alors que les risques climatiques continuent de menacer les moyens de

subsistance des agriculteurs, OKO reste un partenaire inébranlable dans la

protection et le soutien des communautés agricoles du Mali.

Pour plus d'informations et pour garantir votre sécurité pour la prochaine saison,

contactez OKO dès aujourd'hui !

In July 2022, OKO and Allianz started a partnership in Ivory Coast, with the support of the cocoa trading company Touton. OKO brought its crop insurance distribution technology to help the millions of cocoa farmers in Ivory Coast who survive on an average of just $0.78 a day.

Over the course of 6 months, OKO and Allianz conducted 2 pilots in 2 different areas, and brought insurance to 1,500 farmers. Using a soil moisture index developed by AllianzRe, OKO was able to identify if a plantation was in dire situation that would impact its yield. To make sure that this product was available to all farmers, OKO conducted awareness campaign with a team of representatives on the field, and connected with Mobile Money wallets (MTN and Orange) to help farmers pay the registration fee at their own pace. This innovative approach was rewarded on the 1st of March 2023 at the InsurTech Insight conference in London, a major event in the insurance industry.

More than 150 applications were submitted by different insurers, but it is that partnership with OKO that brought the award to Allianz. Marcel Shäheli, representing the partnership, summarised the positive impact of this project on stage: "Instead of having to sell their assets, borrow money, or take their kids out of school to contribute to the household income, farmers now receive financial assistance to support them through challenging climate conditions.”

Going forward, OKO and Allianz will continue this partnership to bring a very much needed safety nets to more farmers in Ivory Coast. And more agro- industries are partnering with OKO to sure the livelihood of smallholder farmers supplying them. Stay tuned for more updates in the coming months!

Insurtech Start-up OKO has closed an extension round of $500,000 USD, and announced their plans to launch in the Ivory Coast with their existing partners, Orange, Allianz and Touton, to bring affordable, low-cost insurance to more farmers in Africa.

The start-up operates in Mali and Uganda, and offers automated insurance using satellite data and mobile payments for farmers whose fields are negatively affected by weather patterns, mainly droughts and floods. Since its launch, OKO brought insurance to more than 15,000 farmers in Mali and Uganda.

OKO saw an impressive 6x growth in the number of paying customers from 2020 to 2021 and is continuing to expand its reach in 2022, with new crops covered, and new partnerships signed with financial institutions providing agricultural loans to insured farmers.

The extension round was made possible by global impact-tech accelerator Katapult, along with three business angels: Guillaume Leenhardt (CEO of Gentle Finance), Henry Allard (CEO of Filhet-Allard Maritime), and Lionel Dorie Founding Partner of Augusta Energy Group).

This announcement follows a recent seed investment in April 2021 of $1.2 million, which was led by by Newfund, ResiliAnce, and Mercy Corps Venture. A month later, OKO launched in Uganda, in collaboration with the Agro Insurance Consortium.

The launch in Ivory Coast will be an opportunity for OKO to collaborate directly with Touton (which invested in April 2021), leveraging Touton's assets and contributing to their efforts in creating a sustainable cocoa value chain. Simon Schwall, Co-founder and CEO of OKO, said; "Ivory Coast has always been a priority market for us, so when we saw the opportunity to launch OKO there this year we jumped on it. We are bringing strong partners to make this expansion a success and we have big ambitions for the months to come."

Commenting on his company’s decision to invest, Fabrice Boullé, Investment Director for Katapult said, “We're thrilled to be partnering with such a high- performing team like OKO. We are a proud investor as they exemplify our philosophy: solving one of humanity's biggest problems, while having a strong

impact, alongside outperforming financial returns. The commercial upside of their solution is important. The impact; even more crucial!”

About Katapult

Katapult is an investment company and a foundation. The investment company focuses on highly scalable impact-tech startups. Katapult currently has 100MUSD under management and has made 138 investments, including 30 direct investments, in startups across 35 countries that are working to implement the UNSDGs.

The Katapult Foundation was established in 2020, gathering all Katapult non- profit initiatives, such as the Accelerate Program, turning tech founders to impact investors, Katapult Future Fest, and the Nordic Impact Investment Network.

About OKO

OKO secures farmers’ income in emerging countries using automated insurance solutions. OKO is accessible to anyone with a phone, and claim payments are automated using satellite data and images. OKO graduated from the Techstars programme in 2018 and was listed in 2020 among the 50 most promising solutions for Financial Inclusion (Inclusive50) by Visa and MetLife foundation.

OKO is active in Mali and in Uganda, with plans to expand to many more

markets in the coming years.